Scaling Services

Export Opportunities: Maritime Infrastructure and Green Corridors

The Middle East’s long history as an energy exporter gives it a head start in developing logistics for hydrogen derivatives. Ammonia, in particular, is a preferred carrier due to its higher volumetric density and existing shipping infrastructure. Green ammonia from NEOM is already contracted for offtake in Europe and Asia, and port upgrades across the Gulf are enabling handling of chilled ammonia and methanol.

Dubai, Sohar, and Yanbu are actively positioning themselves as transshipment hubs for green fuels. The region’s proximity to the Suez Canal enhances its competitiveness relative to Latin American or Pacific exporters, enabling shorter shipping times to European ports.

These ports are also increasingly involved in green corridor initiatives, which aim to decarbonise maritime trade routes through cooperation between origin and destination ports. For Europe, this creates a reliable supply chain for hard-to-decarbonise sectors like shipping and fertilisers. For Gulf countries, it cements their relevance in a future energy landscape where molecules, not just megawatts, matter.

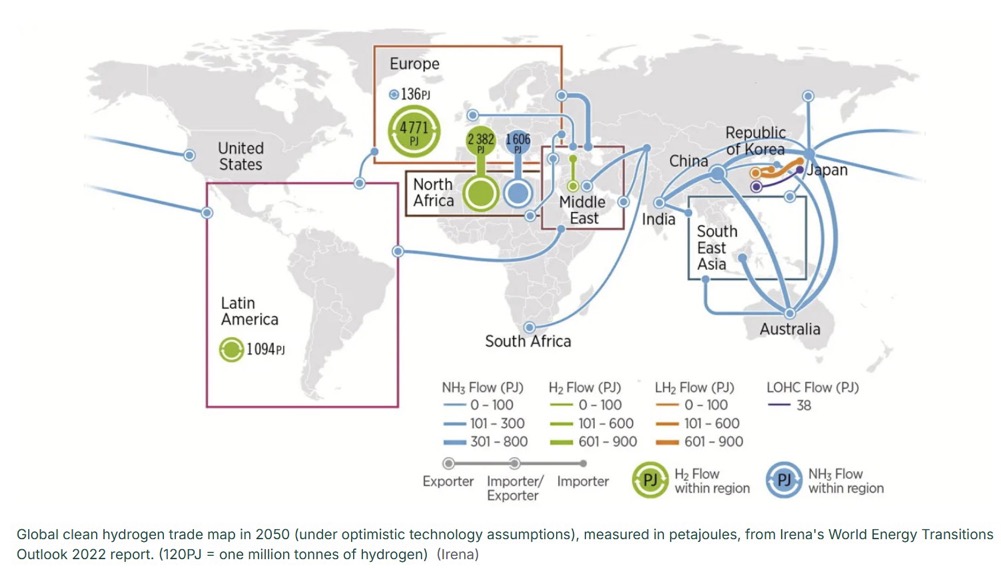

Global Hydrogen and Hydrogen Derivative Trade Map: 2050 (IRENA)

Additionally, she is connected to an extensive network of highly skilled professionals within the Energy sector, enhancing her ability to support and drive impactful partnerships and projects.